A small deposit can feel like a shortcut… until the timeline and risks show up.

You see an untitled block with a “low deposit to secure” offer and it’s easy to think: Why wouldn’t I? Lock it in now, let the market do its thing, build later, job done. And yes, sometimes that play works.

But property doesn’t pay you for optimism. It pays you for the boring stuff: timing, cashflow, contracts, and what happens when the plan doesn’t run on schedule.

This article gives you a straight way to compare return, risk, and time-to-income between buying untitled land and buying an established property. You’ll walk away knowing what questions to ask, what traps to avoid, and which option fits your situation without guessing and without relying on glossy promises.

The quick verdict most buyers miss

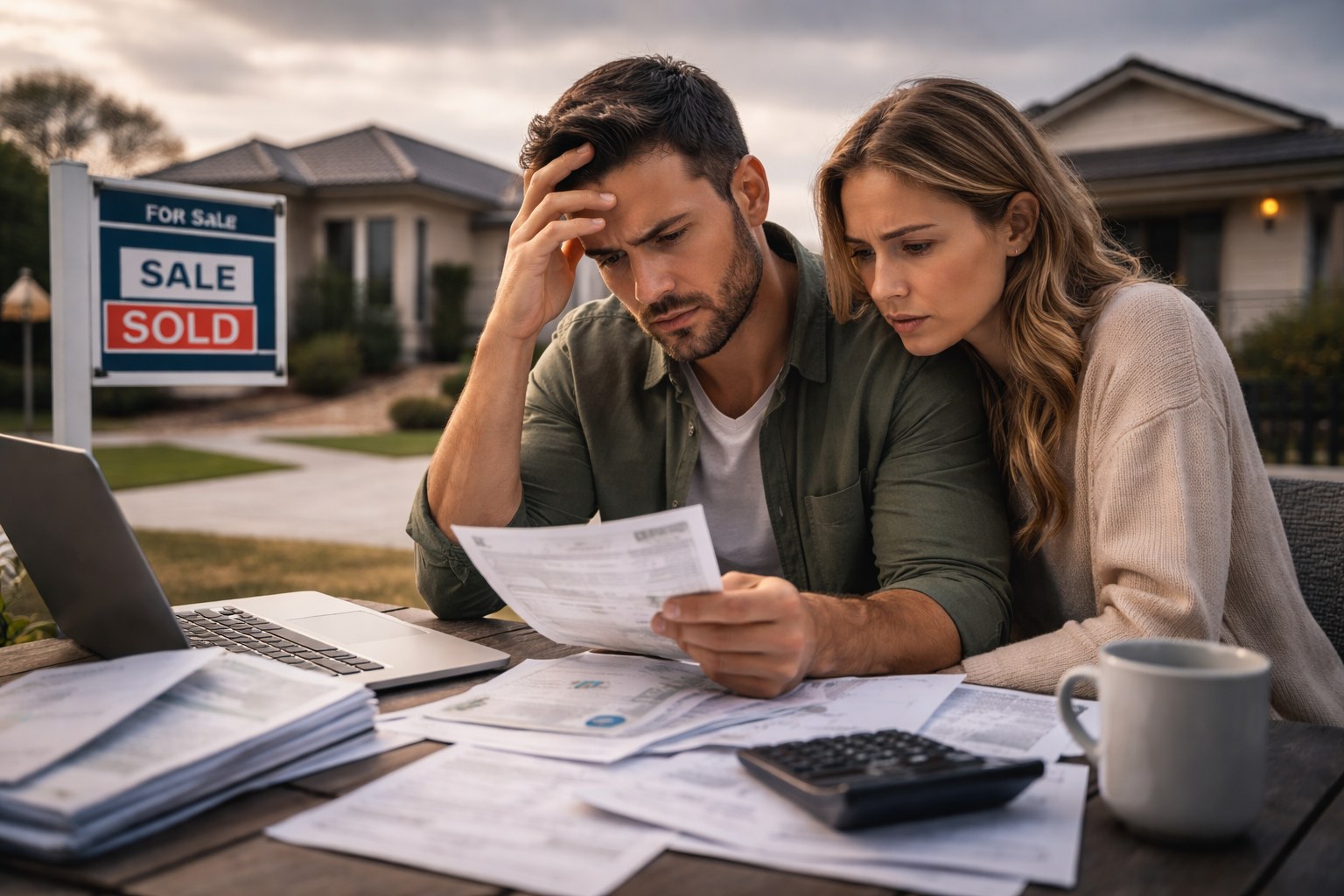

Cheap to secure isn’t the same as cheap to own

A low deposit feels like a bargain because it’s the only number you’re looking at. You “book” the block, get the paperwork, tell your partner you’ve finally got your foot in the door… and it feels like progress.

But booking a deal is the easy part. Finishing it is where the money gets made or lost.

Because between “secured with $30k” and “keys in hand” sits the real bill: settlement funds, stamp duty, holding costs, build price changes, delays, and all the little surprises that don’t show up in the ad. If your plan only works when everything goes perfectly, it’s not a plan — it’s a wish.

The three clocks that decide your outcome

Most buyers compare land and established property like it’s a simple price fight. It’s not. It’s a timing fight. Three clocks control your result:

1) The title clock (when you can settle)

With untitled land, you’re waiting for the block to be registered and ready to settle. That timeline can stretch… or snap forward. Either way, you don’t control it. When the call comes, you need finance ready, not “we’ll sort it out later”.

2) The build clock (when you can move in or rent)

Even after settlement, the home doesn’t exist yet. Build timelines move with labour, materials, approvals, weather, and builder capacity. Every extra month is another month you’re paying without enjoying the property.

3) The rent clock (when income starts)

This is the one most people forget. Established property can start producing income soon after settlement. Untitled land plus a build can mean a long stretch of zero rent while your cash and borrowing capacity are tied up.

Get these clocks wrong and the deal that looked “cheap” can feel expensive fast. Get them right and you’re playing the game with your eyes open.

Titled vs untitled land in plain English

What “titled land” actually means

Titled land is land that’s been officially registered and is ready to settle like any normal property purchase.

In plain terms, it means:

-

The block exists as a legal lot with its own title.

-

The developer’s paperwork is done (the government has registered it).

-

Services are generally in place or approved for connection (think roads, water, sewer, power, NBN depending on the area).

-

You can settle now, and you can usually start building once your plans and permits are sorted.

So titled land is the “ready to go” version. The timeline is clearer, and you’re not waiting for the block to become real on paper.

What “untitled land” really means

Untitled land is land you can sign a contract on today, but you can’t settle yet because the title hasn’t been registered.

You’ve basically bought your place in the queue.

You pay a deposit to secure the block, then you wait while the developer finishes the steps needed to get the title issued. Only after that happens can you settle, and only after settlement can you move on to the next phase (building, renting, or moving in).

This is where people get caught: the price might look good and the deposit feels manageable, but your actual purchase timeline sits in someone else’s hands.

Why untitled land looks so attractive upfront

Lower deposit, bigger headline leverage

Untitled land sells one feeling better than anything else: control.

You put down a small deposit and suddenly you’re “in”. You’re holding a contract on a block worth a few hundred grand, without handing over the full amount today. That gap between what you’ve paid and what you’ve secured is the hook. It feels like you’ve outsmarted the system.

And the story people tell themselves is simple: If the land goes up while I’m waiting for title, I’ve made money on a tiny outlay. Even if the maths is more complicated in real life, the headline still hits hard: “small deposit, big asset”.

Early estate releases and picking better blocks

Getting in early can also mean first pick.

In new estates, the best blocks often go first: a cleaner rectangular shape, better street appeal, a wider frontage, fewer weird easements, or a position that’s quieter and easier to build on. Buyers chase these because they know one thing: when the estate is finished and buyers have choices, the “easy” block usually attracts more attention.

It’s like buying the best seat before the crowd walks in. Same show, but your seat feels a lot nicer.

Building to suit the local renter

Another drawcard is the “build it right” angle. When you start from scratch, you can choose the floorplan, bedrooms, bathrooms, parking, outdoor space — all the features that renters in that area care about.

That can help with rentability, sure. A smart layout and the right inclusions can cut vacancy and reduce tenant turnover.

But here’s the reality check: design is a multiplier, not the engine. If the location doesn’t have steady demand, no floorplan saves you. Location does the heavy lifting; the build just helps you capture the demand that’s already there.

The risks buyers only learn the hard way

Sunset clauses and cancelled contracts

When you buy untitled land, you’re buying a promise with a date attached.

Most contracts include a sunset clause. In simple terms, it sets a deadline for the land to be registered and ready to settle. If that deadline blows out, the contract can be cancelled and your deposit returned.

Sounds fair until you think about the real cost: time.

If your deposit sits parked for 18–36 months while nothing settles, you don’t just lose momentum. You lose options. That same money could have been earning rent, building equity, or helping you buy something else. You get your deposit back, sure, but you don’t get those years back.

Settlement can move faster than your finance

The sales pitch often says “settlement in 18 months”. Then one day you get the email: “Titles are due sooner. Please prepare for settlement.”

If you’re not finance-ready, you can get squeezed.

Banks don’t approve loans based on good intentions. They want current payslips, clean statements, stable employment, and a deal that still stacks up under today’s rules. If your situation has changed, or lending policies tighten, you might be scrambling at the worst possible time.

With untitled land, the developer sets the pace. You need to be ready to run when they say go.

New areas are harder to “data check”

Established suburbs leave footprints. New estates leave brochures.

When an area is still being built out, the data you’d normally use to judge demand can be thin or noisy:

-

lower sales history and fewer comparable results

-

shorter track record for days on market and discounting

-

rental vacancy trends that swing because supply is landing in big waves

On top of that, the shiny future stuff can move. Schools, shops, transport upgrades, even road connections can be delayed or resized. Sometimes plans change completely. If your strategy relies on “what’s coming”, you’re betting on timelines you can’t control.

Exit options can be limited

Here’s the uncomfortable one: if you can’t settle, you might not have an easy escape hatch.

Some contracts restrict nominating the contract to someone else or on-selling before settlement. Others allow it, but with fees, approvals, or conditions that make it hard when you’re under pressure.

This is where people get hurt. Job loss, interest rate jumps, family changes, a lender saying no. Suddenly you need flexibility, and the contract may not give it to you.

Before you sign, get a solicitor to review the contract conditions around nomination, assignment, default, and timelines. You’re not being paranoid. You’re being smart.

The 2026 reality check: building is the bottleneck

Build costs are still rising

If you’re planning to build, you’re stepping into a market where costs are still pushing up, not sliding back to “normal”. Forecasts from quantity surveying groups are still calling mid-single digit construction cost growth across major cities in 2026.

What that means for you is simple: the quote you get early can be the “best case”, not the final number. The longer the gap between signing and starting, the more room there is for surprises.

Delays and builder risk can turn “cheap” into expensive

This is where the low-deposit dream can get ugly.

Every extra month of delay has a price tag:

-

interest and holding costs while you wait

-

months with no rent coming in

-

plan changes, variations, and re-quotes

-

stress you didn’t budget for

And builder risk isn’t theoretical. Construction insolvencies have been running high, with construction among the biggest contributors to insolvency activity.

If a builder folds mid-project, it can mean delays, legal headaches, and a new builder charging more to take over someone else’s half-finished job.

The hidden cost: your borrowing capacity gets tied up

Even if you’ve got cash buffers, lenders still look at an unfinished build as a big commitment.

While you’re waiting for titles, waiting for slab, waiting for frame, waiting for handover, your borrowing capacity can sit in limbo. Banks see a project in motion, costs still uncertain, and rental income still “future tense”. That can slow down your next purchase, even if you’re ready to move.

So when you hear “just buy the land now and build later,” translate it to what it really means: you’re choosing a longer, more fragile timeline. If you’re comfortable with that and funded for it, fine. If not, this is the part that bites.

Why established property often wins on fundamentals

Rent sooner, feedback sooner

Established property is boring in a good way. You settle, you sort the basics, and the home can be advertised for rent straight away. That means income starts sooner, which helps with cashflow and takes pressure off your budget.

You also get fast feedback from the market. If the rent is a touch high, you’ll find out quickly. If demand is strong, you’ll see it in enquiry levels and how fast it leases. Either way, you’re not stuck guessing for 18–36 months while you wait for titles and a build.

You can see what you’re buying

With an established home, you’re buying reality, not a promise.

You can walk the street at 7am and 7pm. You can check the traffic, the noise, the parking, and whether the place feels safe. You can look at nearby homes and see what people actually live like. You can assess school catchments, public transport, and shopping options as they are today.

That visibility matters. It’s harder to get blindsided when you can inspect the asset and the area before you commit.

Land value does the heavy lifting

In property, the shiny parts wear out. Land is what tends to appreciate.

Established homes often have a higher share of their price tied to land value, especially in suburbs with tighter supply. The building might be older, but that can be a feature, not a flaw, because you’re often paying less for “newness” and more for the part that usually drives long-term growth.

Put simply: when you buy established, you’re more likely to be buying what goes up, not what goes out of date.

When untitled land can make sense

The “only if” checklist

Untitled land isn’t automatically bad. It can be a smart move when the conditions are right and you’re funded for the messy bits. Here’s the “only if” checklist I’d want ticked before going anywhere near it:

-

You’ve got real buffers (cash + servicing).

Not “we’ll be fine”. Actual spare cash for delays, rate rises, and build surprises — plus the income to service the loan even if rent is a long way off.

-

The contract terms are buyer-friendly (or at least balanced).

Clear timeframes, reasonable rights if things drag on, and no nasty traps around settlement timing, fees, or your ability to step away. If you don’t understand the wording, you’re not ready to sign.

-

You’re comfortable with a longer timeline and uncertainty.

If waiting 12–24+ months (and sometimes more) would keep you up at night, this strategy will feel like a slow leak in your finances. You need patience and a plan that still works if timelines blow out.

-

The location has genuine demand and limited competing supply.

You want demand that exists now and isn’t relying on “coming soon”. And you want supply that isn’t endless. If thousands of similar blocks and near-identical builds will keep hitting the market, your resale and rent story gets weaker.

If even one of those is shaky, untitled land stops being a strategy and starts being a gamble.

A simple decision framework

Ask yourself these 7 questions

You don’t need a fancy model to make a smart call here. You need honesty, a calculator, and the courage to answer these without wishful thinking.

-

Do I need rental income soon?

If your plan relies on rent to keep you comfortable, untitled land plus a build can stretch that timeline. Established property usually gets income moving faster.

-

If settlement is brought forward, can I still settle?

If the developer says, “Titles are ready earlier,” do you have finance ready now — payslips, buffers, clean statements, and enough deposit?

-

If the build is delayed 12–24 months, can I cope financially?

Don’t ask “will it be delayed?” Ask “what if it is?” If that delay would break you, it’s a no.

-

What’s my contingency for build costs?

If your budget is tight to the dollar, you’re leaving yourself no room for price rises, variations, site costs, or re-quotes. What’s your real buffer?

-

Can I exit if my situation changes?

Job change, family change, lending change. Can you on-sell or nominate the contract, or are you locked in no matter what? If you don’t know, you’re guessing.

-

Is there proven demand today, not just brochures?

Look for evidence: rents being paid now, vacancy trends, how fast comparable homes lease or sell. Promises are not demand.

-

Will this choice help or hurt my next purchase?

Think two steps ahead. Will your borrowing capacity be tied up while you wait for titles and build, or will quick rent and usable equity put you in a better position for the next move?

Answer these straight and the decision usually makes itself.

Due diligence steps before you sign anything

Contract and timing checks

If you’re buying untitled land or a house-and-land deal, the contract is the deal. Read it like your future depends on it — because it might.

Here’s what to check (with a solicitor, not “a mate who bought once”):

-

Sunset date and extensions: What’s the deadline? Who can extend it, how often, and on what grounds? What happens if it runs out?

-

Nomination / assignment rights: Can you transfer the contract to someone else if you need to exit? Is it allowed, restricted, or charged?

-

Deposit terms: How much is due now, when is the next payment due, and where is the deposit held?

-

Inclusions and exclusions: What exactly are you getting? This is where “standard” can quietly mean “bare bones”.

-

Variations and price changes: What can change after signing? Site costs, developer requirements, council conditions, upgrade lists — these are where budgets get chewed up.

-

Settlement triggers: What event triggers settlement, and how much notice do you get? “Short notice” is a stress test on your finance.

If anything feels fuzzy, assume it can go against you until proven otherwise.

Area checks that stop expensive surprises

The suburb will either carry your investment or expose it. Before you commit, sanity-check the demand and the supply.

-

Supply pipeline: How much new land and how many near-identical builds are coming over the next few years? If the area can keep releasing stock, resale can get tougher.

-

Vacancy and rent reality: Don’t rely on “expected rent”. Check what similar homes are leasing for right now and how quickly they’re getting tenants.

-

Comparable rents and sales: Look for true like-for-like comparisons — same bedroom count, similar finish, similar distance to transport.

-

Resale competition: If your future buyer will have 30 similar new builds to pick from, you’ll need to be sharper on price, presentation, and location within the estate.

A few hours of checks now can save you years of regret later.

Closing thoughts

If you only take one thing away, take this: property rewards clean execution.

Untitled land can work, but it asks you to manage more moving parts. Established property tends to be simpler: you settle, rent starts, and you can move on to your next step faster.

If you want help pressure-testing a suburb or comparing scenarios, AbodeFinder can help you run the numbers and look at demand signals like vacancy, rents, and comparable sales so you’re not relying on hope. If you’re reading this on the AbodeFinder blog, you’ll find tools and suburb insights across the site — start there and make your next move with your eyes open.